By Brendan Boyle, Director, Market Intelligence, Transparent Energy, April 2025

In March, the U.S. Energy Information Administration (EIA) released its latest Short-Term Energy Outlook (STEO). From our perspective, the most interesting takeaways from the report are related to the natural gas market – in particular, how forecasts have changed over the past few months.

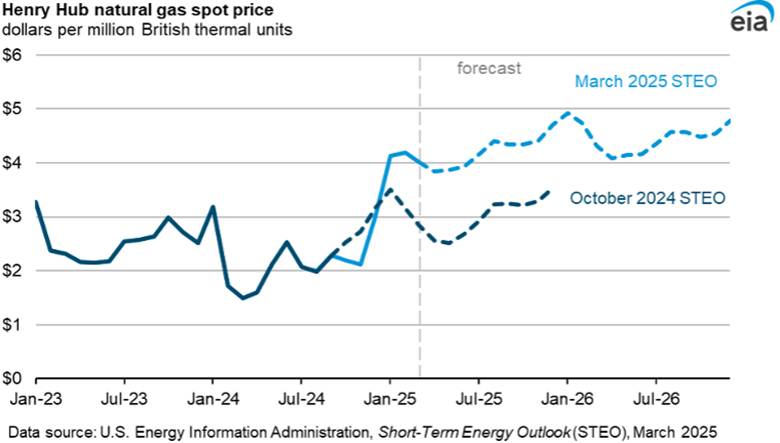

In its October 2024 STEO, the EIA projected that Henry Hub natural gas prices would average $3.10 per MMBtu in 2025. The March report revised that number 35% (!) higher to $4.20 per MMBtu as shown in the chart below.

A major reason for the upward adjustment is that below-normal temperatures in January and February led to increased natural gas consumption. This resulted in much more gas being drawn from storage than expected. U.S. inventories fell from a high of 3,972 Bcf in November to just 1,698 Bcf at the start of March. This 2,274 Bcf drawdown was 25% higher than the previous two winters.

The STEO goes on to project that gas futures will average $4.50 per MMBtu in 2026. As of March 27th, the NYMEX calendar 2026 gas strip settled at $4.39, indicating that the agency expects prices to move even higher over the next year.

Why Are Prices Moving Higher for 2026?

Since July 2024, we’ve seen a steady upward trend in natural gas prices, however, most of the movement has occurred towards the front (i.e., the nearer years) of the forward curve. Calendar years 2027 and beyond have experienced much more modest changes:

| Trade Date | Cal 2025 | Cal 2026 | Cal 2027 | Cal 2028 | Cal 2029 | Cal 2030 |

| 07/29/2024 | $3.24 | $3.63 | $3.71 | $3.64 | $3.59 | $3.50 |

| 03/27/2025 | $4.34 | $4.39 | $3.87 | $3.59 | $3.47 | $3.34 |

| ∆ Change | +34% | +21% | +4% | -1% | -3% | -5% |

Canada also has large projects expected to come online in 2026. Depending on the impact of federal tariffs, our neighbors to the north could begin moving a majority of the 7 Bcf per day currently being sent into the U.S. via pipeline to more profitable markets overseas. Should all these projects progress as expected, the total amount of natural gas that is no longer available for domestic consumption will likely approach 10 Bcf per day – a major hole in available supply – by the end of next year.

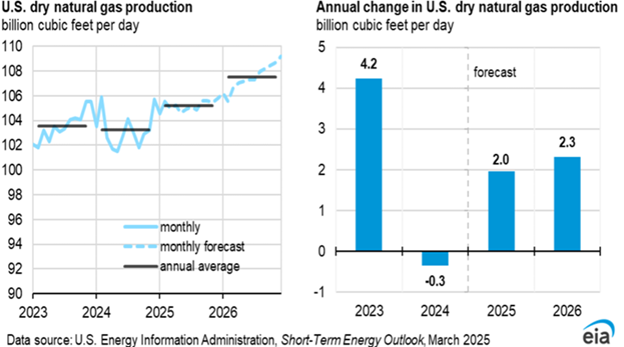

At the same time, U.S. gas production has stagnated. When natural gas prices reached rock bottom in the spring of 2024, production and exploration for gas decreased. Following eight consecutive years of steady growth, we’ve seen a decline in production over the past year:

The EIA is forecasting the return of production growth over the next two years; however, the increase pales in comparison to the expected rise in exports.

Natural gas production companies have made it clear that they are only willing to pull more gas out of the ground when prices meet their acceptable level. What is acceptable? A recent survey of energy companies suggested that the average price needed to incentivize new natural gas drilling was $4.66 per MMBtu – again, higher than today’s prices.

Ok, So Natural Gas Prices are Moving Higher, Does This Affect My Electric Bill as Well?

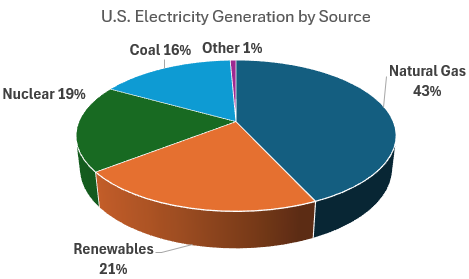

YES! Electricity prices across the country are driven by the cost of natural gas.

Source: EIA

There is a >90% correlation between the price of natural gas and electricity rates across ERCOT, PJM, MISO, NYISO, and ISO-NE, and natural gas consumption in the power generation sector has never been higher.

While the fuel costs to generate electricity continue to rise, demand for power is also on an upward trajectory. New data centers are appearing across the country that host energy-intensive AI technology. There are serious concerns that load growth will substantially outpace the ability of supply to keep up over the next two years. Yes, we’ve heard news of large tech companies looking to rely more heavily on renewables or nuclear power, but wind and solar are intermittent resources and utility-scale nuclear power plants typically take 5-10 years to build with immense capital investment.

What Is the Best Solution for My Business Moving Forward?

The most prudent solution is to begin actively reducing medium-to-long term exposure to price risk. As summer approaches, there will be increasing fears of growing energy consumption nationally – and with them price pressures – based on cooling needs. And continued LNG export growth is likely to cause shortage concerns and more volatile prices.

At Transparent Energy we recognize the dangers of scarcity risk premiums finding their way into the wholesale energy markets, and the impact it could have on our client’s bottom lines. We do not see any meaningful relief for prices in 2025 or 2026, and the opportunity to lock in rates for 2027 and beyond is unlikely to get much more attractive than where those strips are trading today.

Now is the time to act.

***

If you are concerned about rising energy prices and their impact on your business, contact us today at letstalk@TransparentEdge.com.

Categories:

More on News & Releases

-

Tortilla Leader Finds Online Auctions a Tasty Choice for Energy Procurement

04.09.25

La Mexicana Tortilla Factory Drives Down Energy Spend with Transparent Energy; Recommends Company, Process to Tortilla Industry Association Introduction When Rafael Perez, longtime General Manager of La Mexicana Tortilla Factory...

-

Energy Prices Rising Fast: Why a Big Upward Revision Is Raising Concerns for 2026

04.01.25

By Brendan Boyle, Director, Market Intelligence, Transparent Energy, April 2025 In March, the U.S. Energy Information Administration (EIA) released its latest Short-Term Energy Outlook (STEO). From our perspective, the most...

-

Clear and Present Pricing Danger: PJM Capacity-Charge Increases Are Coming Home to Roost

03.24.25

By Keith Jennings, Director, Pricing Desk, Transparent Energy On July 20th, 2024, PJM – the Regional Transmission Organization that manages the electric grid across 13 Mid-Atlantic states – released the...